The first loan you get is always the hardest.

The first loan you get is always the hardest.

After you have taken out multiple loans and paid them all back, banks, credit card companies, and financial institutions are more likely to lend to you. When you have a proven track record of borrowing money and returning it, they come to trust you somewhat.

This makes it easier to get the funds you need when you need them. This is all part of the wonderful experience of “building up your credit.”

All journeys start with a single step, and the journey to good credit begins with that initial loan.

Using your First Loan to Establish Credit

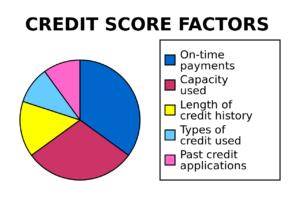

To establish your credit-worthiness you need to borrow money and pay it back on time.

Start small, don’t shoot the moon right off the bat. You will find it easier to manage if you ease into it gently, so start with a small loan of a few hundred bucks.

You will have to fill out some paperwork for these loans, but small dollar loans usually have few hoops to jump through.

Once you have received your funds, you need to pay them back on time. Don’t make the mistake of paying it back too quickly, though. Paying too early is almost as bad as paying too late. When the lender gives you a payment schedule, follow it!

(Except, of course, if you borrow from National Small Loan, where there are no -prepayment penalties. We actually encourage early payment, to save our clients the extra interest. Most lenders do not hold this view.)

Stepping-stone Loans

After that 1st loan is out of the way you have officially taken the first step in your financial journey.

Every subsequent loan is another stepping stone in the path to your future. By careful planning with an eye on the future, you can slowly build up to a much larger loan.

With every loan repaid, you credit will become better and better. Before long you will be able to breeze through the mortgage loan process, because the lenders will see from your credit history that you are credit-worthy.